Description

Section 1 – Introduction to time series data and components of time series models

Section 2 – Estimate simple forecasting methods such as arithmetic mean, random walk, seasonal random walk and random walk with drift

Section 3 – Approximate simple moving averages and exponential smoothing methods with no trend or seasonal patterns such as Brown simple exponential smoothing method.

Section 4 – Approximate exponential smoothing methods with trend and seasonal patterns such as Holt-Winters additive, Holt-Winters multiplicative and Holt-Winters damped methods

Section 5 – Stationary Series & Unit Root test

Section 6 – Importance of differencing

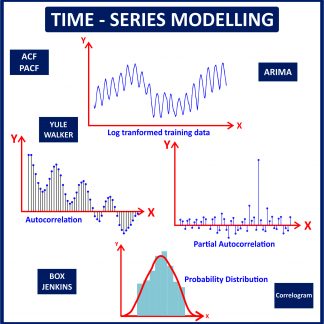

Section 7 – Auto correlation (ACF) and partial auto correlation functions (PACF)

Section 6 – Box Jenkins methods (ARIMA models)/li>

Section 7 – Model diagnostics and residual analysis

Section 8 – Models Forecasting Accuracy

Section 9 – Multivariate Time Series Modelling

Section 10 – Cointegrated Time Series Models

Section 11 – Time Varying Volatility & GARCH/ARCH Models

Section 12 – Recurrent Neural Networks

Section 13 – Long Short Time Memory Neural Networks

Reviews

There are no reviews yet.